Containing health care spending seems to be on everyone’s to-do list, but progress toward that goal has been elusive. Growth in the cost of employer-sponsored health insurance (ESI) has taken no respite in its march upward as employers have shifted more out-of-pocket health costs to their workers. A new California Health Care Foundation survey of participants in California’s employer-based insurance market shows that employers and workers may be reaching their limit on this spending.

Average annual growth in insurance premiums for employer-sponsored health plans exceeded inflation and economic growth rates in 2017, according to the latest California Health Care Almanac on this topic. As in previous years, average premium growth (4.6%) surpassed the rate of inflation (3%) and the growth of the California economy (3%). The average cost of a health plan for a family in California now tops $19,200 a year — a staggering sum equal to almost 30% of California’s median household income. Because California employers pay an average of 73% of their worker’s health premiums, less money is available to increase wages, expand businesses, or create jobs.

These financial pressures have inspired companies offering ESI to search for ways to lower costs and reduce the growth of premiums. One strategy is to use financial incentives to reward employees for making sound decisions about what care to get and where to get it. Very common examples include the use of:

- Copays — set amounts an individual must pay before visiting a doctor or filling a prescription.

- Coinsurance — a percentage of the total cost of a visit or procedure that an employee is responsible for.

- Deductibles — a specified sum of money that a member must pay before insurance will pay a covered claim.

A Worthwhile Trade-Off?

Plans with deductibles larger than $1,300 for single coverage and $2,600 for families are known as high-deductible health plans (HDHPs). These plans allow employers and workers to pay lower monthly premiums in exchange for agreeing to satisfy larger annual out-of-pocket costs before a health plan starts paying for medical care and prescription drugs. Last year, the average family premium for high-deductible coverage in California was $1,500 a month, more than $100 less than the average for all plans. For families with HDHPs, the tradeoff was a $4,449 average annual deductible — far higher than the average for a non-HDHP plan.

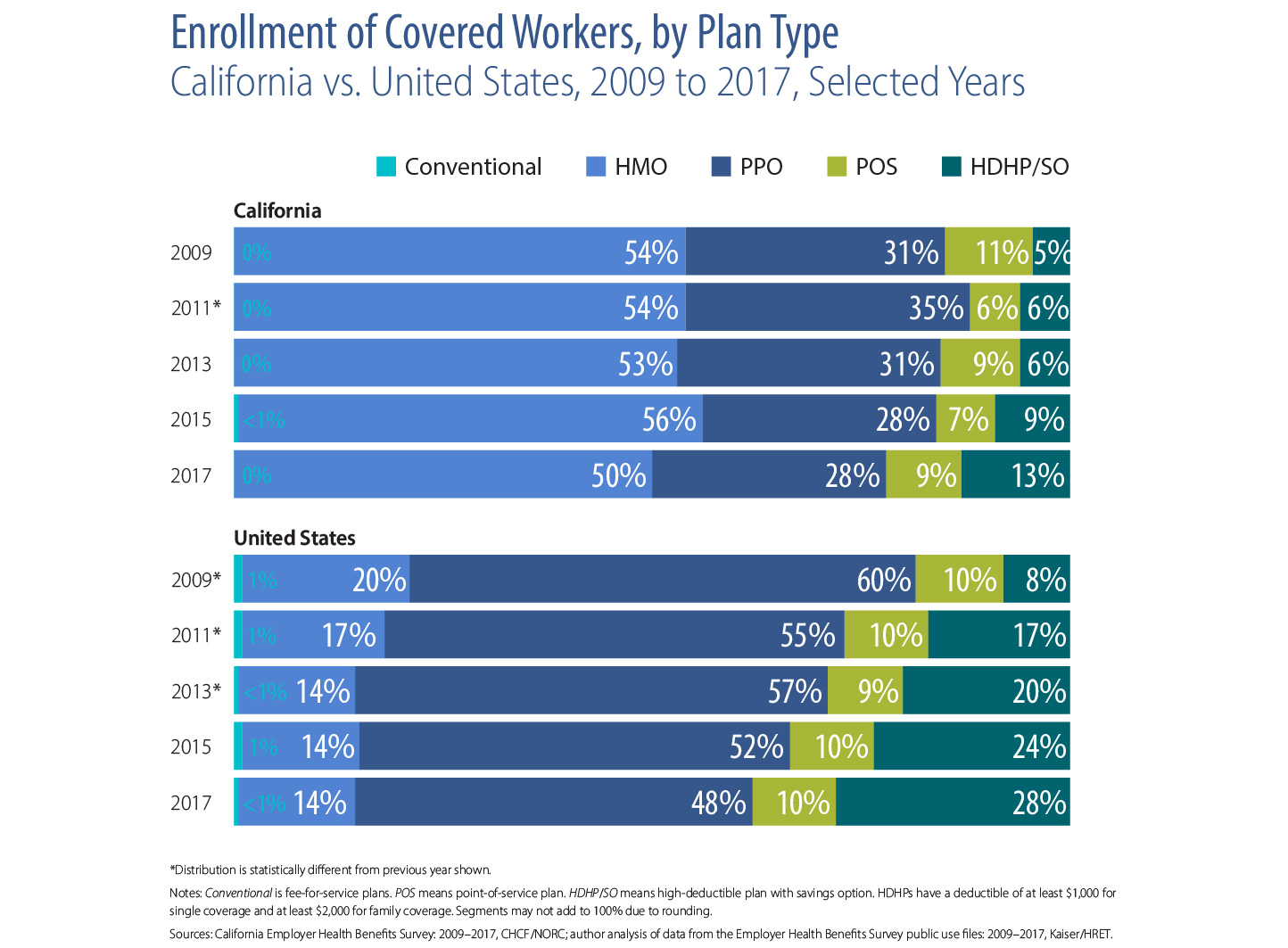

Compared to other states, California’s ESI market has a relatively low rate of covered workers choosing high-deductible policies. In 2017, only 13% of California’s 6.7 million workers with ESI were enrolled in an HDHP option. While the proportion has more than doubled in only four years, it still lags far behind the comparable national rate. Despite the higher premiums, Californians with job-based coverage are much more likely to be enrolled in health maintenance organizations (50%) or preferred provider organizations, known as PPOs (28%).

Firms and workers in California show less enthusiasm for large deductibles than those in other states. Among employees with PPO coverage, average deductibles in California run nearly 20% below the national average despite the relatively high cost of care in the state. As in other parts of the country, the proportion of California workers with PPO coverage and a deductible over $500 continues to climb, but it is still only about half the national rate.

This theme surfaces in California employers’ planning as well. When asked about the likelihood of making certain changes next year, 37% of companies report being very or somewhat likely to raise premiums, 10 percentage points higher than last year. Meanwhile, 28% plan to increase deductibles, compared with only 15% that said they plan to raise workers’ coinsurance or copay amounts.

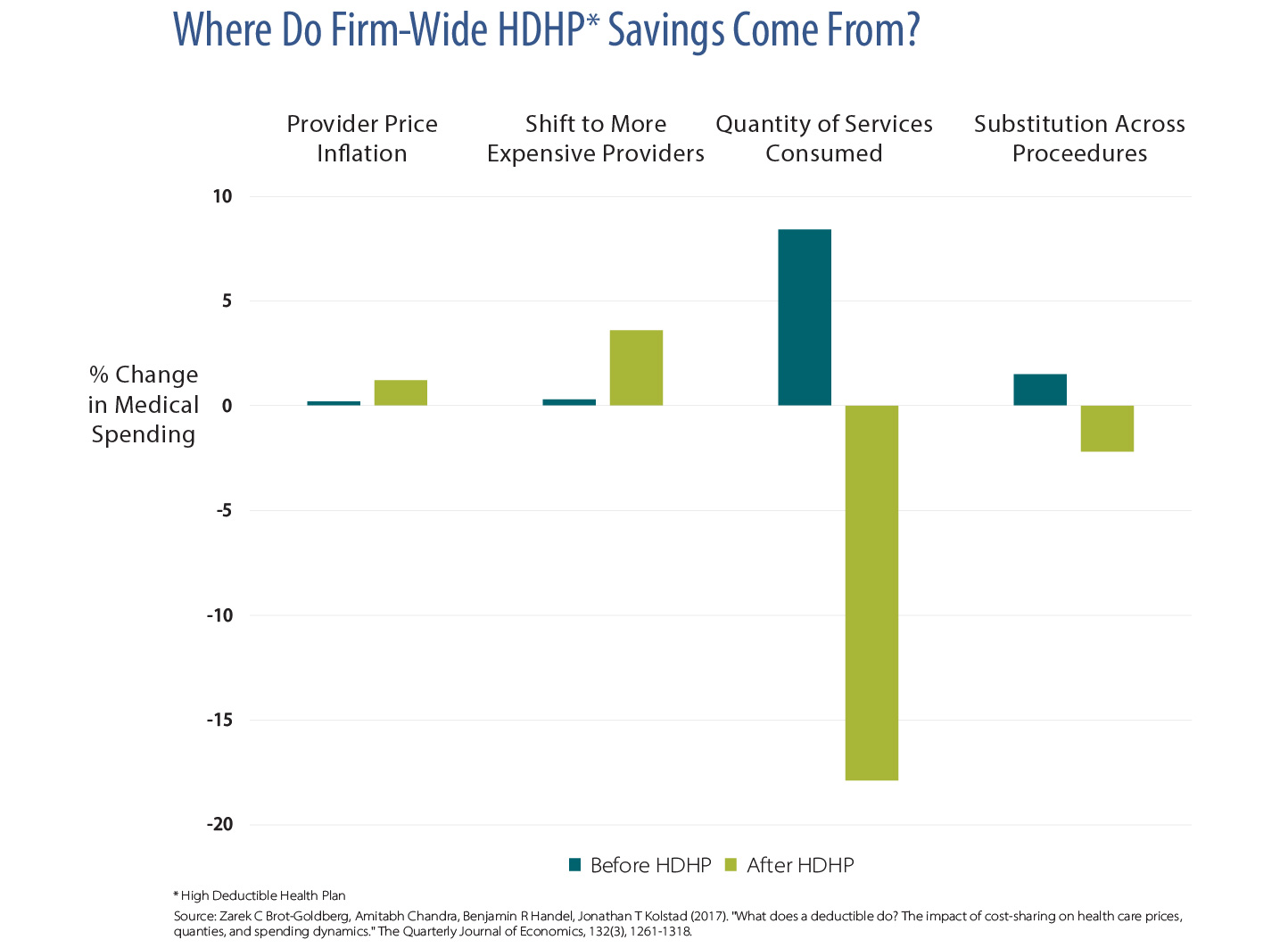

Why might there be less enthusiasm for cost-containment strategies that rely exclusively on large out-of-pocket costs for consumers? Employers may see it as a questionable long-term cost-control strategy. Most academic research shows that while HDHPs do immediately lower total spending, they do so by reducing use of care — and not just unnecessary care. Across-the-board reductions in use of services conflict with chronic care management and population health strategies. They do not effectively target the spending problems that plague the American health care system, most of which are driven by unit price rather than volume of services.

For most employees, the immediate reduction in costs associated with less comprehensive coverage is an undesirable trade-off. A recent national survey found employees preferred more comprehensive insurance over cheaper plans that do not cover everything they need.

This is not to say that California employers have abandoned consumer-focused strategies in efforts to improve value. The large supermarket chain, Safeway, introduced a successful consumer-focused benefit design that gives employees an incentive to price-shop for imaging and lab tests; California Public Employees’ Retirement System (CalPERS) has done the same for orthopedic surgery. Walmart, Lowes, and McKesson waive copays and deductibles for employees receiving services from a pre-screened set of providers that deliver low-cost, high-quality care.

Financial Penalties Aren’t the Only Cost-Control Strategy

Employers’ experience engaging consumers offers important lessons for future efforts to make the health care system more affordable. First, consumer financial incentives are powerful and need to be carefully deployed. This is particularly true for consumers with low incomes, who are more likely to forgo necessary care when faced with larger copays, coinsurance, and deductibles. These out-of-pocket costs function as financial penalties. Positive incentives for seeking medically necessary, high-value care can be part of a more effective cost-control strategy.

Second, if consumers are expected to shop for the best value for treatments and services, they need transparent information on price and quality. The information is most helpful when it includes bundled total out-of-pocket costs for shoppable tests and procedures. And finally, as in other industries, health care markets only function effectively when choice exists among competing suppliers. Individual consumers attempting to price shop in a monopolistic environment will not achieve greater success than large purchasers equipped with far more negotiating leverage.

Like any cost-control strategy, using consumer-based financial incentives has both potential and limitations. Our Almanac data on California’s job-based insurance market suggests that while total costs continue their seemingly inexorable march upward, employers and employees are reaching their limit when it comes to the use of blunt financial barriers to restrain health care spending.

Authors & Contributors